Understanding Financial Stress Australia: Beyond Income Brackets

It’s easy to think that if you’re earning a good salary in Australia, you’re automatically set when it comes to money. Like, you’ve crossed some invisible finish line and financial worries are a thing of the past. But honestly, that’s not always the case. Plenty of people with impressive paychecks find themselves feeling the pinch, stressed out about their finances. It turns out, income level is only one piece of a much bigger puzzle.

The Illusion of Financial Security for High Earners

So, why do people making good money still get stressed about finances? It’s a bit of a head-scratcher, right? Well, a lot of it comes down to expectations and how we manage what we earn. Just because the bank account looks healthy doesn’t mean the money isn’t already spoken for, or that there aren’t big financial goals looming. It’s like having a fancy car but no idea how to drive it – you have the potential, but not necessarily the control or the roadmap.

Common Triggers of Financial Strain in Affluent Households

What actually causes stress for people who earn more? It’s often not about not having enough, but about managing what they do have. Think about these things:

- Lifestyle Creep: You get a raise, so you buy a nicer car, a bigger house, or start taking more expensive holidays. Before you know it, your spending has gone up right along with your income, leaving little extra.

- Investment Worries: High earners often have investments, which is great. But markets go up and down. Seeing your portfolio shrink, even temporarily, can be a real source of anxiety, especially if you’re relying on that money for future goals.

- Big Life Changes: Things like divorce, unexpected health issues for yourself or a family member, or even helping adult children can put a massive strain on finances, no matter how much you earn.

The Psychological Impact of Financial Worries

Money stress isn’t just about numbers in a spreadsheet. It messes with your head. When you’re constantly worried about money, even if you have a lot of it, it can lead to:

- Anxiety and Sleep Problems: You might find yourself tossing and turning at night, replaying financial scenarios in your head.

- Relationship Strain: Money arguments are super common, and they can put a real damper on relationships with partners, family, or friends.

- Reduced Well-being: Constant financial worry can make you feel generally unhappy, less motivated, and even impact your physical health over time. It’s like a heavy cloud that follows you around.

Factors Fueling Financial Stress in Australia

It’s easy to think that if you’re earning a good wage, money worries are a thing of the past. But that’s just not the reality for a lot of people in Australia, even those doing well on paper. Several things are making it tough to feel financially secure these days.

Rising Cost of Living Pressures

Everything just seems to cost more, doesn’t it? Groceries, petrol, rent – the list goes on. Even with a decent salary, these everyday expenses can eat up a surprising chunk of your income. It feels like you’re constantly playing catch-up, and that can be really stressful. You might be cutting back on things you used to enjoy, or putting off bigger purchases, just to make ends meet. It’s a constant balancing act, and it wears you down.

Investment Volatility and Market Uncertainty

Many Australians rely on investments, whether it’s superannuation, shares, or property, to build wealth and secure their future. But the market can be a wild ride. One minute things are looking up, the next they’re down. This unpredictability can cause a lot of anxiety, especially if you’re nearing retirement or have big financial goals. Seeing your hard-earned money fluctuate can make you question your financial decisions and worry about whether you’ll have enough when you need it.

Unexpected Life Events and Emergency Funds

Life has a funny way of throwing curveballs when you least expect them. A sudden job loss, a serious illness, or even just a major home repair can put a massive strain on your finances. If you don’t have a solid emergency fund in place, these events can quickly lead to debt. It’s not about being unprepared; it’s about acknowledging that life happens. Having a buffer can make all the difference between a temporary setback and a full-blown financial crisis.

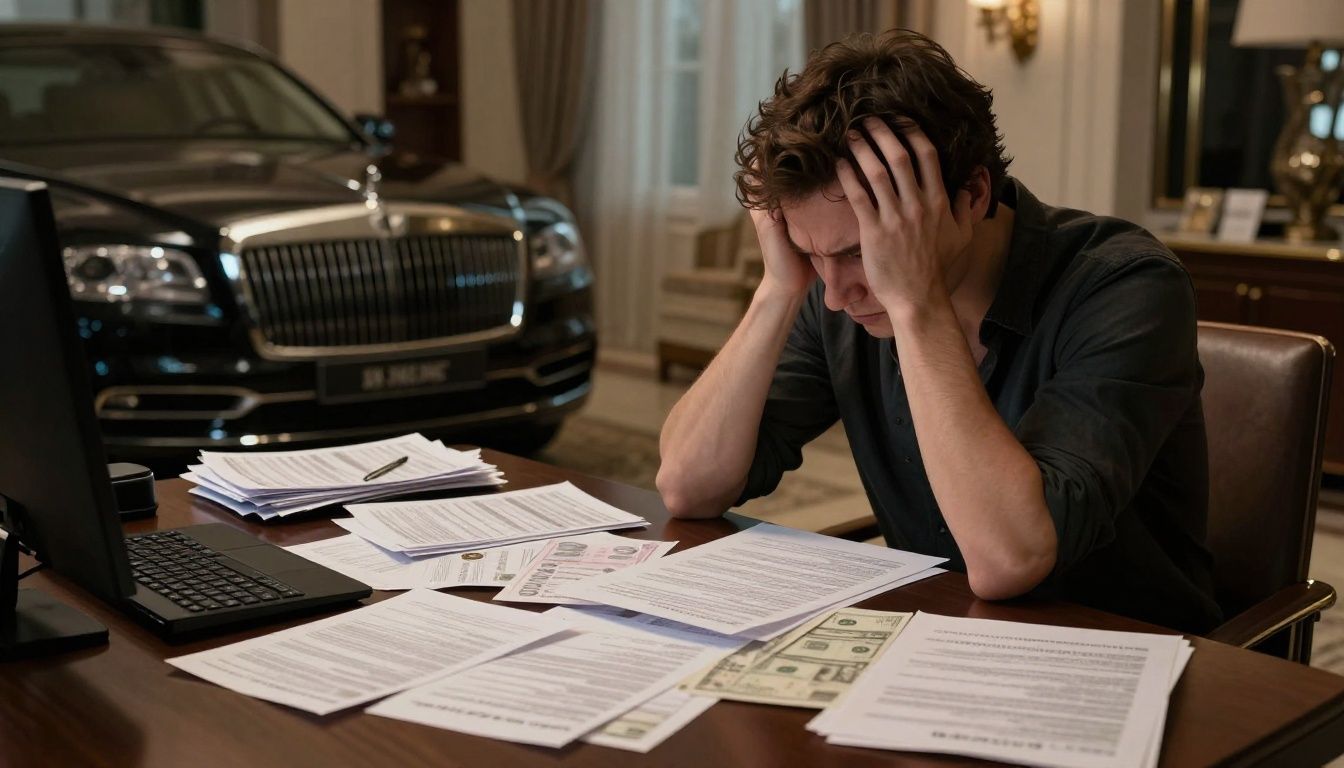

The High Earner’s Dilemma: Lifestyle Creep and Debt

It might seem counterintuitive, but earning a lot of money doesn’t automatically mean you’re financially secure. For many high earners in Australia, the opposite can be true. As income rises, so do expenses, often without us even noticing. This is what we call ‘lifestyle creep,’ and it’s a sneaky trap that can leave even the most successful people feeling financially strained.

The Trap of Escalating Expenses

Think about it. When you first started earning more, maybe you upgraded your car, moved to a nicer neighbourhood, or started taking more frequent holidays. These aren’t necessarily bad things, but they add up. Suddenly, that comfortable salary is just covering the basics, and there’s not much left over for savings or unexpected costs. It’s like running on a treadmill that keeps speeding up – you have to keep working harder just to stay in the same place. We often justify these increases by saying we ‘deserve’ them, but without a conscious effort to control spending, these desires can quickly outpace our income growth.

Mortgage Burdens and Investment Property Debt

For many Australians, property is seen as the ultimate investment. High earners often take on significant mortgages for their primary residence, and then, wanting to build wealth, they might take on more debt for investment properties. While this can be a smart move, it also means a lot of money is tied up in loans. The monthly repayments can be substantial, and if interest rates go up, or if a property sits vacant, that ‘asset’ can quickly become a major financial burden. It’s easy to get caught up in the idea of property as a guaranteed path to riches, but the reality of managing multiple mortgages and the associated costs can be a huge source of stress.

The Pressure to Maintain a Certain Image

There’s a subtle, and sometimes not-so-subtle, pressure that comes with being a high earner. You’re expected to live in a certain type of house, drive a certain type of car, and participate in certain social activities. This can lead to spending money not because you genuinely want or need something, but because you feel you should. It’s about keeping up appearances, which can be exhausting and financially draining. This external pressure can make it hard to say ‘no’ to expensive outings or purchases, even when your budget is already stretched thin. It’s a cycle where you earn more, spend more to fit in, and then feel stressed about not having enough saved, even with a high income.

Strategies to Mitigate Financial Stress Australia

Okay, so we’ve talked about how even folks with good incomes can feel the pinch. It’s not just about earning more; it’s about managing what you have. Let’s get into some practical ways to dial down that financial worry.

Developing a Robust Financial Roadmap

This sounds a bit formal, but honestly, it’s just about having a clear map for your money. Think of it like planning a road trip – you wouldn’t just hop in the car and hope for the best, right? You’d figure out where you’re going, how much gas you’ll need, and where you’ll stop.

- Know Your Numbers: Seriously, sit down and list out everything coming in and everything going out. No hiding from those bills or that daily coffee run. Seeing it all laid out is the first step.

- Set Clear Goals: What are you actually saving for? A new car? A holiday? Retirement? Having specific targets makes it easier to stay on track. Vague goals like ‘save more’ are easy to ignore.

- Budgeting That Works for You: Forget those super strict, impossible budgets. Find a system that fits your life. Maybe it’s an app, a spreadsheet, or even just a notebook. The key is consistency.

Building and Maintaining an Emergency Fund

This is your financial safety net. Life throws curveballs, and having money set aside means a leaky roof or a sudden job loss doesn’t have to become a full-blown crisis. It’s about peace of mind.

- Start Small, Be Consistent: Don’t feel like you need to save thousands overnight. Even putting away $20 or $50 a week adds up. The habit is more important than the initial amount.

- Keep it Accessible (But Not Too Accessible): You want to be able to get to this money if you really need it, but it shouldn’t be mixed in with your everyday spending account. A separate savings account is usually best.

- Aim for 3-6 Months of Expenses: This is the general rule of thumb. It sounds like a lot, but remember, you’re building it over time. Adjust this based on your personal situation and job security.

Diversifying Income Streams and Investments

Relying on just one source of income or one type of investment can be risky. If that one thing falters, you’re in a tough spot. Spreading things out can make your financial situation more stable.

- Side Hustles: This doesn’t mean you need to start a massive business. It could be freelancing a skill you have, selling crafts, or even renting out a spare room. Anything that brings in a little extra cash.

- Investment Variety: Don’t put all your eggs in one basket. Talk to someone about different investment options – shares, property, bonds, etc. The goal is to have different things that perform differently in various market conditions.

- Skill Development: Sometimes, the best way to diversify income is to improve your main job skills or learn new ones. This can lead to promotions, better pay, or new career opportunities that bring in more money.

Seeking Guidance for Financial Well-being

Sometimes, even with the best intentions, managing your money can feel like trying to solve a puzzle with missing pieces. That’s where getting some outside help can really make a difference. It’s not a sign of weakness; it’s a smart move to get your finances on track, especially when things feel complicated or stressful.

The Benefits of Financial Coaching

Financial coaching is a bit different from advising. Coaches focus more on your habits and behaviors around money. They can help you:

- Build Better Money Habits: This could mean creating a budget that actually works, sticking to savings goals, or reducing unnecessary spending.

- Understand Your Money Mindset: Sometimes, our beliefs about money get in the way of our goals. A coach can help you identify and change those patterns.

- Stay Accountable: Having someone to check in with can be a powerful motivator to stick to your financial plan.

- Develop Practical Skills: You might learn how to track your spending more effectively, plan for future expenses, or manage debt more efficiently.

Navigating Complex Financial Situations

Life throws curveballs, and sometimes they hit your finances hard. Dealing with things like:

- Unexpected Job Loss: This can be a huge shock. A coach can help you figure out your immediate next steps and how to adjust your budget.

- Significant Debt: Whether it’s credit card debt, personal loans, or investment property loans that are causing worry, professionals can help you create a plan to tackle it.

- Inheritance or Windfalls: Receiving a large sum of money can be exciting but also presents its own set of challenges. Getting the knowledge on how to manage it wisely is important.

- Business Ownership: If you own a business, managing personal and business finances can get tricky. Expert guidance can keep things separate and optimized.

Getting professional help isn’t about admitting you can’t handle your money. It’s about recognising that sometimes, a little expert knowledge can save you a lot of stress and help you build a more secure future.

Cultivating a Healthy Relationship with Money

It’s easy to get caught up in the numbers – the balances, the interest rates, the investment returns. But money is more than just digits on a screen. It’s tied to our feelings, our security, and our dreams. Building a better connection with your finances isn’t about deprivation; it’s about making conscious choices that align with what truly matters to you. Think of it like tending a garden. You wouldn’t just throw seeds around and hope for the best, right? You prepare the soil, choose the right plants, water them, and weed out the bad stuff. Your money deserves that same kind of care.

Mindfulness and Financial Awareness

This is about paying attention to where your money goes without judgment. It’s not about guilt-tripping yourself for that impulse buy, but rather noticing the patterns. Start by tracking your spending for a month. You might be surprised where your cash is actually going. Is it a lot of small coffees? Or maybe subscriptions you forgot about? Just observing can be the first step to making changes. It’s like realizing you’ve been driving with the parking brake on – once you notice it, you can let it go.

Setting Realistic Financial Goals

Big goals are great, but they can feel overwhelming if they’re too far out of reach. Break them down. Want to buy a house in five years? That’s a big one. What about setting a goal to save a specific amount for a down payment in the next 12 months? Or maybe your goal is simpler, like paying off a credit card in six months. Having smaller, achievable targets gives you a sense of accomplishment along the way, which keeps you motivated. It’s like climbing a mountain – you focus on reaching the next base camp, not just the summit.

Prioritizing Financial Health Over Material Wealth

This is a tough one, especially when society often links success with possessions. But true financial health isn’t about having the biggest house or the fanciest car. It’s about having peace of mind, knowing you can handle unexpected expenses, and having the freedom to make choices that aren’t dictated by debt. It means asking yourself: “Does this purchase truly add to my life, or am I just trying to keep up?” Sometimes, the most freeing thing you can do is decide that you have enough.

Conclusion

Financial stress can affect anyone, regardless of income level. By understanding the common triggers, developing a solid financial roadmap, and seeking professional guidance when needed, you can gain control over your finances and reduce anxiety. Don’t let financial worries hold you back. Schedule a call with Andrew today to discuss your financial goals and create a pathway for a more secure future with the knowledge that you can navigate any financial challenge that comes your way.

Book your free Smart Investor Call and let’s start growing your wealth – one smart step at a time.