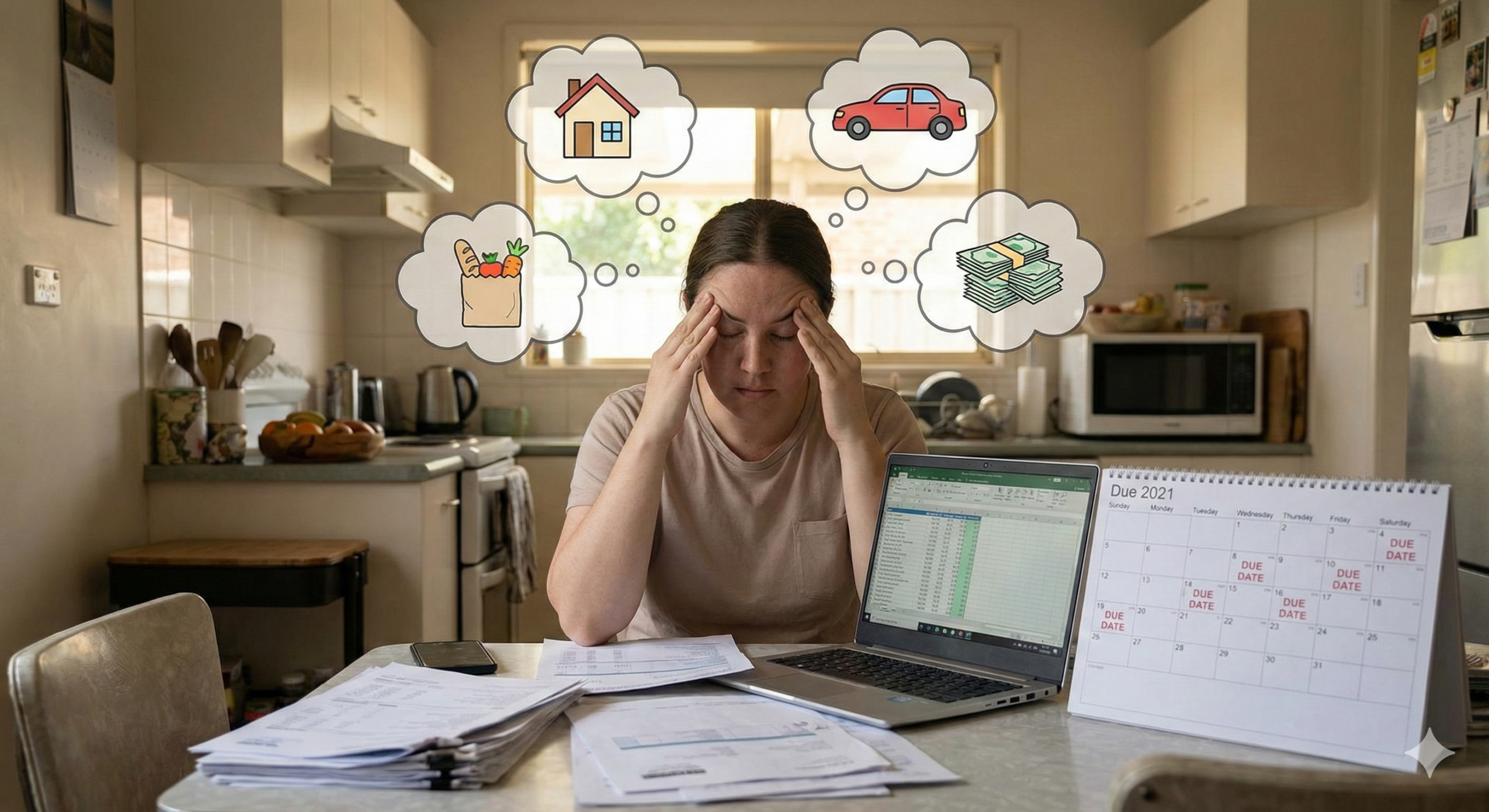

Money mental load is the invisible job that many Aussies and families do every day, and it is exhausting.

It is not just paying the bills. It is the constant thinking. Remembering due dates. Worrying about rates. Planning for school costs. Guessing if the grocery bill will blow the week. Thinking about Christmas. Thinking about the car rego. Thinking about the next dentist visit. It is the mental tab that never closes.

And here is the sneaky part. Even when the dollars are fine, the money mental load can still feel heavy. Because the stress is not only about numbers. It is about responsibility, safety, and being the one who has to know.

What is the “money mental load” really?

The mental load talk got popular because people realised that running a home is not just chores. It is also planning, noticing, and managing.

Money is the same.

Someone has to notice when the power bill is higher. Someone has to plan for the school fees, excursions, lunches and uniforms. Someone has to remember the insurance renewal. Someone has to decide if you can afford a weekend away without wrecking the month.

If you have ever laid in bed doing money maths in your head, you know exactly what this is.

This load becomes heavier when life is busy. Kids. Work. Rising costs. A surprise repair. A health bill. A job change. A family member who needs help.

The load is not a personal failure. It is a system problem.

Who usually carries the load, and why?

In many couples, one person becomes “the money person”. Sometimes it happens by choice. Sometimes it happens by default.

It can look like this.

One person pays bills, checks accounts, does the budget, and thinks ahead. The other person says, “You’re better at that stuff.”

Or the opposite.

One person avoids money because it feels scary, confusing, or shameful. The other person picks it up because someone has to.

Over time, the money mental load sticks to the same person like glue.

This is not about men versus women. It can be either. What matters is the pattern.

If one person holds the knowledge, they also hold the stress.

If one person avoids, they also miss the feeling of control and confidence.

That gap can turn into resentment.

How the Money Mental Load Shows Up at Home

This is the part people don’t talk about enough. The money mental load does not stay inside a spreadsheet. It leaks into everyday life.

It shows up as snappy comments in the supermarket. As silent worry when the kids ask for something small.

It shows up as a partner feeling judged, even if nobody said anything. As one person feeling alone, because they are carrying a secret job.

It shows up as two people arguing about small purchases when the real issue is bigger.

It also shows up as avoidance. If money chats always end in tension, you stop having them. Then things get worse. Then the tension grows. Then the next chat is even harder.

It becomes a loop.

But loops can be broken.

The two money roles that cause most friction

Most couples fall into one of two roles, even if they do not mean to.

The Carrier.

This person tracks everything. They remember. They plan. They worry. They might also control, because control feels safer.

The Avoider.

This person stays out of it. They might say they trust the Carrier. They might feel embarrassed. They might feel like they always get it wrong.

Both roles are understandable. Both roles create friction.

The Carrier feels unsupported. The Avoider feels criticised.

And the relationship starts to feel like a parent and a child, not two adults building a life.

The fix is not “try harder”. The fix is structure.

The real goal: shared clarity, not perfect budgeting

A lot of families think the answer is a strict budget.

Sometimes budgets help. Sometimes they make people feel trapped.

The real goal is shared clarity.

Shared clarity means both adults can answer these questions without panic.

What money is coming in? What must be paid next? What can we spend this week? What are we building toward?

When both people have clarity, the money mental load drops fast. Not because life is cheaper, but because the thinking is shared.

And when the thinking is shared, the relationship feels safer.

Simple structural solutions that actually work

Here are simple systems that reduce the money mental load without turning your life into a finance hobby.

First, set a weekly money huddle.

Pick a day and time. Ten to fifteen minutes. Same time each week. Put it in your calendar like a school pickup.

You look at three things only.

What bills are due before the next huddle.

What your spending limit is for the week.

One small win you will do next, like moving money into savings.

Second, make money visible.

If only one person can see the numbers, only one person can relax.

Choose one place where the truth lives. It could be a shared notes app. It could be a simple spreadsheet. It could be a budgeting app.

The tool matters less than the habit.

Third, automate what you can.

Auto pay your key bills. Auto move savings on payday, even if it is small.

Automation is not lazy. It is mental health.

Fourth, name the roles without shame.

Instead of “you never care about money”, try “I feel like I’m holding the money mental load alone.”

Then agree on who owns what. Not forever. Just for this season.

One person can own bill payments. The other can own checking the plan each week.

Both must be involved in big choices.

Fifth, use a simple rule for spending.

Make a weekly spending number that is guilt free. When it is spent, it is spent.

This stops daily money micro fights.

It also stops one person playing police.

A script for the awkward money conversation

If money chats have been tense, you need a softer start.

Try this.

“I want us to feel like a team with money. Lately it feels heavy, and I don’t want it to sit on one person. Can we try a short weekly money check-in for a month and see if it helps?”

That sentence does three important things.

It talks about teamwork. It names the feeling. It offers a small trial, not a forever change.

Small trials feel safe. Safe feels doable.

What financial freedom looks like

Financial freedom is not just a big number.

For a family or a single, it often looks like this.

More calm at home.

Less fear when a bill arrives.

More choice about work.

More room to help your kids and still protect your future.

More space to enjoy your life now, not “one day”.

When the money mental load is shared, you make better decisions. You save more. You waste less. You fight less.

That is not fluffy. That is practical.

Your next step this week

Do not try to fix everything at once.

Pick one structure.

If your house is stressed, start with the weekly money huddle.

If your house is unclear, start with making money visible.

If your house is overwhelmed, start with automation.

Then do it for four weeks.

Four weeks is long enough to feel a shift. Short enough to feel possible.

And when you feel that shift, you will realise something important.

Money mental load is not “just how it is”.

It is something you can design.

And when you design it together, you move closer to financial freedom and a home that feels lighter.

And there ends the cousnelling session ha ha.

Book your free Smart Investor Call and let’s start growing your wealth—one smart step at a time.